Resisting Federal Monetary Policy through States' Rights: Lessons from California's Experience During the Civil War

This article is free, but features "Premium Research" content available through bitcoin lighting micropayments. Download a lightning-enabled wallet, like Cash App, to participate in this #Value4Value experience, powered by mash.com.

Introduction

States are rediscovering their monetary sovereignty. As interest in the concept of "states' rights" reaches an all-time high, states are exploring bills to limit the use of the federal government's proposed central bank digital currency, or CBDC.

CBDCs are fully digital currencies issued directly by central banks to citizens. Like paper dollars, CBDCs are central bank liabilities. But unlike paper dollars, which provide high levels of financial privacy, CBDCs undermine the individual right to privacy by giving "the federal government complete visibility into every financial transaction by establishing a direct link between the government and each citizens’ financial activity."

CBDCs combine this mass surveillance capability with programmability, creating the frightening potential to restrict purchases of certain goods and services to achieve policy goals (for example, preventing SNAP recipients from buying alcohol; rationing gasoline, propane, or even meat to fight climate change; imposing spending limits on ammunition or prohibiting the purchase of certain types of firearms; preventing spending on reproductive health or medical marijuana/psychedelics). CBDCs will also give the central bank levers of fine-tuned economic control, by, for example, incentivizing spending or saving at the individual level through dollars with expiration dates.

In other words, CBDCs are a central planner's dream come true. Indeed, the CCP in China is pioneering them.

Both Florida and South Dakota have asserted their sovereign powers over trade and commerce within their borders to resist this application of federal power over money. Specifically, both states have opposed amending their respective commercial codes to include new definitions of "money" proposed in the Uniform Commercial Code (drafted by a private body of attorneys and lawmakers that crafts model codes to promote uniformity across states). The governors of these two states believe the proposed amendments will pave the way for CBDCs by including government-issued digital currencies in the definition of "money", while at the same time excluding non-governmental digital currencies like Bitcoin.

The governor of Florida, Ron Desantis, has advocated for a law that would preclude recognizing CBDCs as "money" in Florida's commercial code. As his office explained it:

The legislative proposal protects consumers and businesses from a federally controlled CBDC by:

Expressly prohibiting the use of a federally adopted Central Bank Digital Currency as money within Florida’s Uniform Commercial Code (UCC).

Instituting protections against a central global currency by prohibiting any CBDC issued by a foreign reserve or foreign sanctioned central bank.

Calling on likeminded states to join Florida in adopting similar prohibitions within their respective Commercial Codes to fight back against this concept nationwide.

And Governor Kristi Noem of South Dakota vetoed the UCC amendments passed by the state's legislature, stating her belief that the amendments "open[] the door to the risk that the federal government could more easily adopt a CBDC, which then may become the only viable digital currency."

I have returned HB 1193 with my VETO.

— Governor Kristi Noem (@govkristinoem) March 10, 2023

The bill adopts a definition of “money” to specifically exclude cryptocurrencies. But these revisions do include Central Bank Digital Currencies as money.

These developments concern me for several reasons, which are found in this letter: pic.twitter.com/3eqzdI80if

While the amendments certainly would "make a CBDC easier to use for purposes of the UCC," as the Cato Institute explains, "that is still not to say a CBDC is being created through the UCC." Moreover, as Professor Carla Reyes has pointed out, the UCC amendments actually seek to "preserve the negotiability of bitcoin ... in a way that should better enable individuals to freely transact in bitcoin without worry that they are taking the bitcoin subject to a secret lien." And, at the end of the day, a CBDC will still be legal tender under federal law, capable of discharging any debt, regardless of state commercial codes.

So, if states wish to insulate their economies and citizenry from the pernicious effects of CBDCs and promote financial freedom, focusing on the UCC is not the best policy.

This article proposes another solution. A mostly forgotten episode of monetary history offers a blueprint for states that wish to limit the spread of a federal CBDC. Not since the Civil War have states asserted their rights over monetary matters so forcefully. And no, I'm not talking about the confederacy. During the Civil War, California and Oregon effectively seceded from the monetary Union created by the "greenbacks" (paper fiat legal tender), yet remained in the political Union in the war against the confederacy. This was achieved through a combination of private contractual provisions and supportive legislative actions.

Monetary Secession, Political Union

In 1862, Congress passed the Legal Tender Act, authorizing the issuance of non-interest-bearing United States notes that were not redeemable in gold or silver specie, but were nonetheless "legal tender in payment of all debts, public and private, within the United States, except duties on imports and interest." (That the federal government still mandated gold for payment of duties demonstrates that it continued to value hard money, it just didn't have enough to wage a total war.) These notes came to be called "greenbacks."

This was not the first instance of fiat paper money in the Republic (as I have detailed here). But it was the first time fiat had been issued by the federal government since the ratification of the Constitution. And it was also the first time the federal government declared anything other than gold and silver legal tender.

Indeed, the constitution does not grant Congress an express power to declare legal tender. This power was first read-in to the constitution by the Supreme Court under the rationale that it was expedient during a time of war. But, as is often the case, temporary powers assumed by the government in times of crisis prove to be permanent. In 1884, the Supreme Court declared that paper fiat greenbacks issued after the war had ended were constitutional.

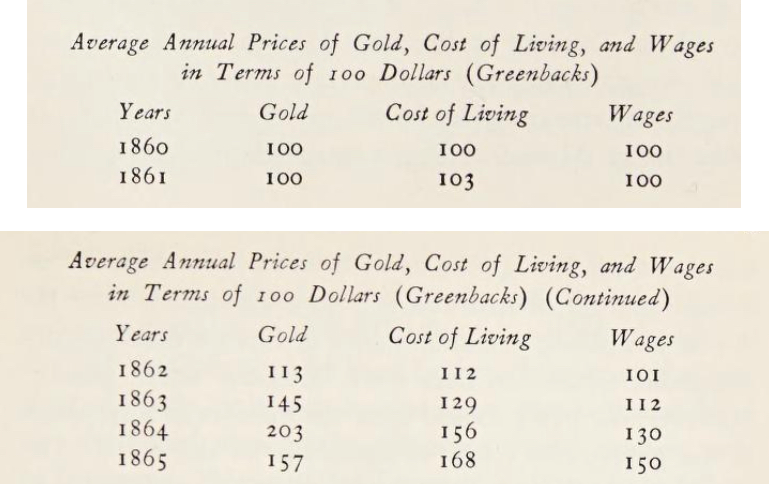

The inflationary effect of fiat money on the Union states was felt almost immediately after the greenbacks were issued in 1862.

In California, between June 13 and June 30th, 1862, the discount on greenbacks rose from 1-2% to 8%. By July the discount reached 15%. This new, inflationary currency only confirmed Californians' deeply held belief in hard money. Due to the gold rush, Californians used gold in their day-to-day lives. In fact, California's constitution forbade banks from issuing notes in California. Banks could only custody gold deposits.[1]

Despite its disdain for the federal government's fiat paper, California stayed loyal to the Union, and its courts recognized the greenbacks as constitutional legal tender.[2]

California merchants, however, forcefully resisted greenbacks. In San Francisco, meetings were held during which the majority of the merchants and businesses agreed not to accept greenbacks – and to blackball anyone that did. "Greenback" became a derogatory slur for anyone who attempted to discharge an honest debt with the depreciated paper ("Greenback Smith", "Greenback Johnson", etc.).[3]

Merchants then formalized their preference for gold by inserting gold clauses into their contracts, which provided for payment in gold or its equivalent. By operation of private contract, a tender of greenbacks was not recognized.

Without a law recognizing the validity of such clauses, however, the courts would not enforce them. Thus, the California legislature passed the "Specific Contract Act," which directed courts to enforce gold clauses through "specific performance" by requiring delivery of the gold as stated in the gold clause, rather than merely entering a money judgment for an amount of dollars.

The operative provision of the Specific Contract Act read:

In an action on a contract or obligation in writing, for the direct payment of money, made payable in a specified kind of money or currency, judgment for the plaintiff, whether the same be by default or after verdict, may follow the contract or obligation, and be made payable in the kind of money or currency specified therein.

The Specific Contract Act simply recognized and enforced the right to contract for payment in any kind of money or currency agreed to between freely consenting parties. In the absence of a gold clause (or any other clause specifying kind of money for payment), greenbacks would be the default. Because the law merely acknowledged freedom of contract, and did not discriminate between types of money, it was able to skirt the constitutional scrutiny (the law didn't even reference greenbacks). The California Supreme Court upheld the Specific Contract Act in 1864.

Oregon, Nevada, and Idaho followed California's lead and passed their own versions of the Specific Contract Act. Through the combination of private contractual provisions and legislative action, these western states were able to maintain their gold standard despite the federal government issuing paper fiat legal tender.[4]

As Murray Rothbard observed:

This experience illustrates a continuing problem in contract law: It is not sufficient for government to allow contracts to be made in gold or gold coin. It is necessary for government to enforce specific performance of the contracts so that debtors must pay in the weight or value of the gold (or anything else) required in the contract, and not in some paper-dollar equivalent decided by law or the court.[5]

Find the Bitcoin Brief valuable? Return some value by tapping the "Donate" button. Or subscribe for free.

A Sly, Roundabout Way: State Laws Promoting Financial Freedom.

What lessons can be learned from California's triumph over greenbacks?

California’s Specific Contract Act did not directly challenge federal legal tender law. Instead, it merely created a remedy in state courts for contractual claims that sought to enforce choice of payment. Financial freedom, backed by states' power to set contract law and court procedure, proved to be a "sly, roundabout way" to take money out of the hands of the federal government.

Direct state bans on a federal CBDC are not likely to succeed. To be sure, some courts (the Sixth Circuit Court of Appeals and Western District of New York) have upheld state laws that proscribe the method of payment for certain services (in both cases, scrap metal sales). But those courts reasoned that the state laws specifying a method of payment did not violate the constitution's prohibition on state legal tender laws because the allowable methods of payment were still convertible to federal legal tender (checks, for example).

In contrast, a CBDC is not just a promise to pay legal tender, it is itself legal tender. Recall, CBDCs are direct liabilities of the central bank, just like dollar bills. A state law restricting acceptance of CBDCs in discharge of debts would encroach on the federal government's supreme powers over legal tender.

Thus, any law designed to limit CBDCs must do so obliquely. The California Specific Contracts Act did not mention gold, silver, greenbacks, or any other type of money. The law simply let freely contracting parties determine the type of payment for themselves. By facilitating freedom of choice in payments, states can promote a range of alternatives to CBDCs (including Bitcoin) through the natural market process.

That means, to be successful, any such legislation must support a pre-existing market of circulating CBDC alternatives. Oregon, Nevada, and Idaho all had circular gold-based economies. The legislatures of those states did not mandate a gold-standard or the prohibition of greenbacks, but simply backstopped the private market innovation of gold clauses with judicial recognition and enforcement.

Bitcoiners must continue growing adoption and building out circular bitcoin-based economies. By including bitcoin clauses like the gold clauses of the west, bitcoiners can ensure payment in their preferred medium of exchange. Below, sample bitcoin clauses are offered as Premium Research content, based on actual gold clauses tested in court.

And states should pass legislation requiring courts to enforce bitcoin clauses (or any clauses specifying type of money for payment) through specific performance. That means entering judgments requiring debtors to deliver the specified amount of bitcoin, rather than entering money judgments in dollar terms, which could be discharged by the use of legal tender, i.e., CBDCs. Below, sample legislative language is offered as Premium Research content.

The Feds Strike Back?

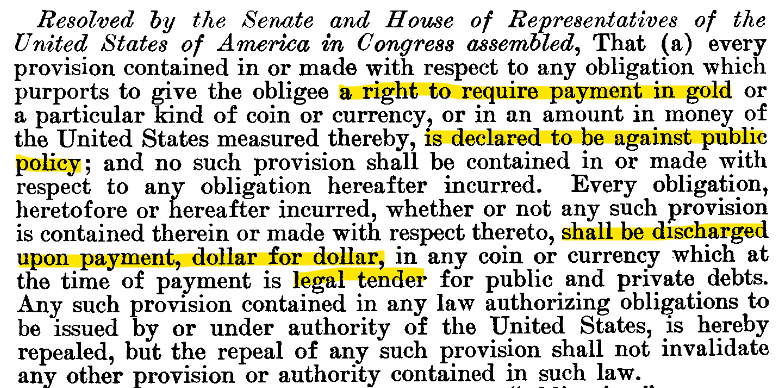

Although successful in maintaining the gold-standard during the Civil War, the various state Specific Contract Laws were ultimately rendered dead-letter by the Roosevelt administration's war on gold at the outset of the great depression.

Many bitcoiners are familiar with FDR's April 5, 1933 Executive Order 6102 criminalizing private possession of gold. (Indeed, Bitcoin's pseudonymous creator listed his birthday as April 5th.) Less well-known, however, is Congress's joint resolution of June, 1933, which invalidated all gold clauses as contrary to public policy:

When Congress's abrogation of gold clauses reached the Supreme Court in a series of cases known as the Gold Clause Cases, it was one of the most anticipated and divisive decisions in U.S. history:

The decisions received significantly more coverage in the [New York] Times than did other major New Deal cases. For perspective, the number of articles devoted to them more closely resembles that of historic moments like the moon landing or 9/11 attacks than it did other major Supreme Court decisions such as Roe v. Wade. The phrase ‘‘gold clause’’ appeared in more Times articles (49) on the day after the decisions than did ‘‘poultry,’’ (10) ‘‘minimum wage,’’ (19) and ‘‘abortion’’ (15) combined, on the days after Schecter, West Coast Hotel, and Roe.[6]

The Gold Clause Cases almost sparked a constitutional crisis. In anticipation of a decision declaring the gold clause abrogation unconstitutional, FDR prepared a draft "fireside chat" in which he would announce his intent to ignore the Supreme Court and implore the nation to do the same. [7] And the New York Times reported that "Government officials and members of Congress 'were studying the possibility of increasing the membership of the Supreme Court from nine to eleven or twelve.'" [8] (The Supreme Court and FDR were frequently in conflict during the New Deal, and the Gold Clause Cases presaged the "court packing plan" and the "switch in time that saved nine"). Ultimately, to avoid a crisis, the Supreme Court backed down and upheld Congress's abrogation of gold clauses.

Would Congress similarly attempt to force acceptance of CBDCs by nullifying bitcoin clauses in all public and private contracts? While the Gold Clause Cases provide the federal government the legal precedent for such a maneuver, practically speaking, it would need a convergence of circumstances to pull it off.

First, and foremost, CBDCs would need to be in circulation. It is unclear when, if ever, the federal government will turn to a fully digital dollar. And the consensus appears to be that the Federal Reserve would need congressional approval before issuing a CBDC.

Second, the country would have to be deep in economic crisis and the federal government would have to feel that its CBDC is threatened. FDR's attack on gold was acceptable due to the worsening depression. Gold was an easy scapegoat for poor central bank policy.

Third, the executive and legislative branches would have to be closely aligned. FDR had the support of a majority of the Senate and House; the president essentially dictated whatever legislation he wanted. This scenario seems unlikely to occur in our modern polarized, hyper-partisan times.

Fourth, and finally, the federal government would need a subservient Supreme Court, or at least a Supreme Court prepared to make a "strategic retreat." [9]. Although the Gold Clause Cases are binding precedent, this current Supreme Court is not shy about overturning precedent the majority views as wrongly decided. It is possible the Supreme Court, if presented with a bitcoin abrogation clause case, would uphold the fundamental right to freedom of contract (especially because the Gold Clause Cases are broadly viewed as analytically weak).

For now, therefore, it appears bitcoin clauses and Specific Contract Laws are safe from federal preemption. But any of the above circumstances are subject to change. States and bitcoin advocates should act now while conditions are favorable. If the shield of financial freedom and states' rights is erected before the Federal Reserve issues a CBDC, the American populace will be much less tolerant of draconian bans on alternative monetary assets, like Bitcoin.

Now is the time to work towards policies that will actually slow, and perhaps prevent, centralized overreach into our financial lives.

Premium Research

If you'd like access to the following sample contract clauses and legislative language, just tap the "Premium Research" button and pay the bitcoin lighting invoice that pops up with your lighting wallet.

If you don't have a lighting wallet or bitcoin, download Cash App and buy a few dollars in the "money" tab. Then tap the QR scanner in the top right of the "Bitcoin" screen and scan the QR code displayed on the invoice after tapping the "Premium Research" button.

These samples are for discussion and educational purposes only and do not constitute legal advice.

Sample Bitcoin Clauses

The California Supreme Court in Lane v. Gluckauf held that the following clause triggered the Specific Contracts Law:

I promise to pay ... the sum of $2843 in gold coin of the standard value of 1860 of the United States of America ... and if said principal and interest is not paid in gold coin ... then I promise ... to pay ... in addition thereto and as damages, such further amount and percentage as may be equal to the difference in value in the San Francisco market between such gold coin and paper evidence of indebtedness of the States or of the United States, that are or may hereafter be made a legal tender in payment of debts by the laws of this state or the United States.

In contrast, the California Supreme Court in Reese v. Stearns held that a clause merely requiring payment in gold or its equivalent

did not trigger the Specific Contracts Law, because it provided no standard of camparison between gold dollars and paper dollars. This issue of determining the amount of gold to be paid in the contract is unique to the situation in 1862, where two types of dollars circulated using the same unit of account (gold coin dollars comprising a specific weight, and paper greenbacks). The gold clauses did not, therefore, specify a weight of gold to be paid, but instead specified a standard gold dollar value as of a certain time and place (in the above example, 1860 and San Francisco).

Bitcoin, on the other hand, has its own unit of account (which is divisable into smaller units of 100,000,000 satoshis per bitcoin), and so a bitcoin clause would not require reference to a specific conversion rate. For example, a bitcoin clause could simply state:

payment shall be made in bitcoin in the amount of 10,000,000 sats (0.10 btc)

Such a clause is straightforward. But it's useful only if both parties are already on a bitcoin standard and denominating expenses, liabilities, products, and services in bitcoin. What if one or both parties are not yet on a bitcoin standard?

In that case, the parties could use a variation of the clause in Lane v. Gluckauf:

payment shall be $2750 in bitcoin of the standard value of [date of agreement], and if said payment is not paid in bitcoin then I promise to pay, in addition thereto and as damages, such further amount as may be equal to the difference between $2750 in bitcoin of the standard value of [date of agreement] and bitcoin of the standard value as of the date of tender.

Under this variation of bitcoin clause, if $2750 would buy 10,000,000 sats (0.10 btc) on the date of the agreement, then 10,000,000 sats will discharge the debt. If, on the date of tender, the price of bitcoin has increased in U.S. dollar terms such that 10,000,000 sats is now worth $3000, the debtor/obligor could not discharge the debt for $2750 in U.S. dollars. A dollar tender would, in fact, be a breach of the agreement, entitling the creditor/obligee to damages amounting to $2750 plus the difference in the value of bitcoin between the date of the agreement and date of tender. This would make the creditor/obligee whole, in bitcoin terms (they could go purchase 10,000,000 sats with the $3000).

These examples are merely a starting point for discussion purposes, based on research into historical gold clauses (and are not legal advice; consult an attorney before using any of the above). The purpose of these clauses is to be compatible with Specific Contracts Laws, as proposed below. Please contact me with thoughts, critiques, or variations on these bitcoin clauses. I am interested in learning how bitcoin businesses are currently structuring their contracts, and whether current practice would trigger application of Specific Contracts Laws.

Sample Legislative Language

California's Specific Contracts law stated:

In an action on a contract or obligation in writing, for the direct payment of money, made payable in a specified kind of money or currency, judgment for the plaintiff, whether the same be by default or after verdict, may follow the contract or obligation, and be made payable in the kind of money or currency specified therein.

A few tweaks are required to reflect modern judicial procedure and clarify the intent:

In an action on a contract or obligation for the direct payment of money, made payable in a specified kind of money or currency, judgment for the plaintiff shall be entered in the kind of money or currency specified therein. Nothing herein shall be construed to preclude a plaintiff's right to seek specific performance for the delivery of the kind of money or currency specified in the contract or obligation.

This proposed language removes the requirement that a contract be in writing (as oral agreements are recognizable under law), thereby broadening the scope of any modern Specific Contract Law.

The language also subsitutes "may" for "shall" in its directions to the courts, as "may" in modern usage is permissive and would afford too much discretion to the courts to enter judgments that did not follow the contract.

And the language is more specific about what a court is to do, i.e., enter a judgment in terms of the currency or money agreed to by contract. This would confer on the plaintiff a money judgment, not just an order to tender the contracted-for currency. A money judgment is executable against other assets of the judgment-debtor and comes with additional safeguards for judgment-creditors (like bonds pending appeal).

Finally, although this proposed language would, by default, result in a money judgment, it includes language clarifying that a plaintiff can still seek specific performance of a contractual provision for payment in a specific kind of money. This gives the plaintiff the option in their complaint to seek both a money judgment and, in the alternative, an order granting specific performance, compelling the judgment-debtor to hand over the specific type of money. This option may be preferable under certain circumstances, and a Specific Contracts Law should maintain that common law right while also guaranteeing a right to a money judgment in money other than dollars.

Again, this example is merely a starting point for discussions (and does not constitute legal advice). The goal is to prevent money judgments on bitcoin contracts being denominated and enforced in CBDC dollars. By instructing courts that they must enter judgment in the type of money specified by contract, individuals who wish to opt out of a federal CBDC can do so while maintaining protections under state contract law.

Please reach out to me with comments, questions, suggestions and critiques to the proposed language. Lets work together towards policies that will actually slow, and perhaps prevent, centralized overreach into our financial lives.

Footnotes

[1] A History of the California Supreme Court, 1850-1879, Vol. 14 J. Cal. S. Ct. Hist. Society 461 (2019)

[2] Id. at 467

[3] Michael Timothy Caires. (2014) The Greenback Union: The Politics and Law of American Money in the Civil War Era [doctorcal dissertation; University of Virginia] at 262.

[4] Murray Rothbard, A History of Money and Banking in the United States: The Colonial Era to World War II, 129-30 (2002);

Caires at 270;

Arthur Nussbaum, Money in the Law National and International: A Comparative Study in the Borderline of Law and Economics, 585 (1950).

[5] Rothbard at 129

[6] David Glick, Conditional Strategic Retreat: The Court's Concession in the 1935 Gold Clause Cases, The Journal of Politics Vol. 71, No. 3 (July 2009) at 805]

[7] Gerard Magliocca, The Gold Clause Cases and Constitutional Necessity, 64 Fla. L. Rev. 1243, 1262-64 (2012)

[8] Glick at 807

[9] See generally id.