Introducing the Legal Tender Series

This is the first post in a four-part article exploring the constitutionality of state-level Bitcoin legal tender laws — and the philosophical arguments against such laws.

This post was originally published on March 31, 2022

- Part I: Introduction and Summary of the Argument

- Part II: The Originalist Case for State-Level Bitcoin Legal Tender Laws.

- Part III: The Textualist Counter-Argument.

- Part IV: Bitcoin’s Faustian Bargain.

Introduction

Tender Trending

El Salvador's "Ley Bitcoin," declaring Bitcoin legal tender [1], kicked off a groundswell of support for similar laws internationally and in the United States.

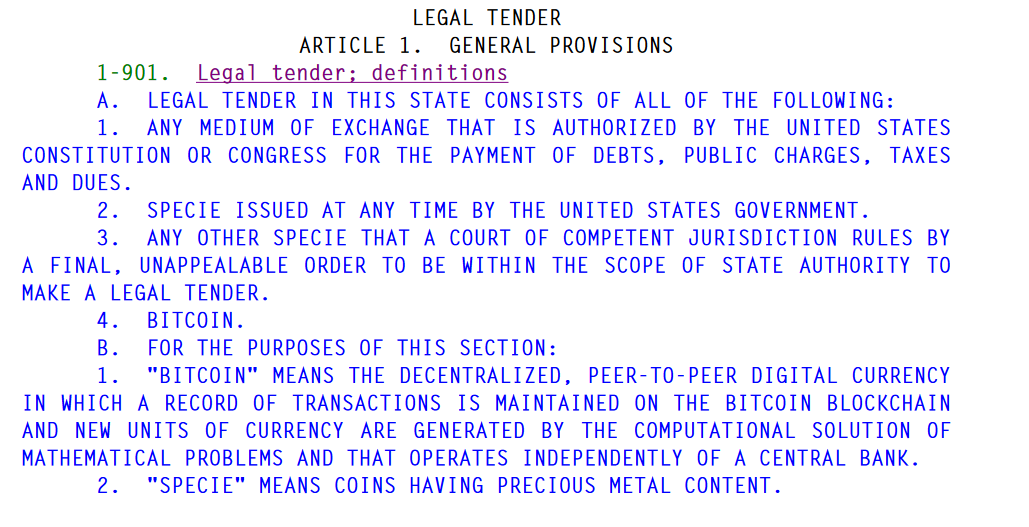

Governors of Colorado and New Hampshire are exploring Bitcoin-related laws. The legislatures of Arizona and California have introduced bills addressing the use of Bitcoin in some way.[2] California would let Bitcoin (and other cryptocurrencies) be used to pay taxes. And Arizona's proposed bill goes even further, expressly declaring Bitcoin (and only Bitcoin) legal tender within the state[3]:

Savvy politicians and candidates are seeking to curry favor with Bitcoiners by making bold proclamations about working to make Bitcoin legal tender:

And Bitcoiners are cheering on these efforts as newly minted "single-issue voters":

Over 1,300 messages have been sent to Federal and State officials to defend #Bitcoin in the first 24 hours of launching this tool.

— Dennis Porter (@Dennis_Porter_) February 3, 2022

Legal Tender letter: https://t.co/ATcsxa0xCN

Support COMPETES letter: https://t.co/2V0PBq5XFQ

Single Issue Voter letter: https://t.co/lkkr5dyDuZ

But what does it even mean to make a money "legal tender"? What benefits or advantages would accrue to Bitcoin under this status?

The answer, legally speaking, is not much.

Legal Tender Defined

In its modern sense, "[l]egal tender is money which, if tendered by a debtor in payment of his debt, must not be refused by the creditor."[4] That’s it.

In other words, legal tender laws force a creditor to accept a certain type of money if offered by the debtor to extinguish the debt — even if the original contract called for payment in a different money. Thus, legal tender status only applies to debts, not spot transactions like the exchange of goods and services. Just because the U.S. dollar is legal tender "for all debts public and private" doesn't mean that Starbucks is required to accept it as payment, if it chooses not to. Legal tender status alone will not compel a barista to accept Bitcoin for your latte.

For that, a subspecies of legal tender laws is required: the compulsory tender law. El Salvador adopted this framework, where all providers of goods and services in spot transactions are barred from refusing Bitcoin. [5]

But spot transaction mandates have not been part of the Anglo-American conception of tender laws since the nineteenth century.[6]

So, under the modern definition of the law, it simply grants a debtor the right to discharge their debts with the legal tender money. There's not much to get excited about there.

Perhaps, then, those advocating for Bitcoin legal tender laws are misinformed about the scope of tender status, and believe it will bring other benefits (like removal of capital gains taxes). Or, perhaps, they believe that by achieving this status, Bitcoin will gain an aura of legitimacy, which will then spur further adoption.

The Constitution Ignored

Whatever the rationale behind this recent push for legal tender status, one fundamental obstacle has been overlooked.

The U.S. Constitution prohibits states from passing legal tender laws.

Article I, Section 10 contains a list of prohibitions on the states:

No State shall . . . coin Money; emit Bills of Credit; make any Thing but gold and silver Coin a Tender in Payment of Debts; pass any. . . law impairing the Obligation of Contracts."

Few passages of the Constitution are as explicit as this. Article I, Section 10 seems to put an end to the discussion of state legal tender laws regarding Bitcoin. States cannot make anything legal tender except for gold and silver. Bitcoin is neither gold nor silver.

But Bitcoin does share many of the same characteristics as gold. In fact, it’s a lot better than gold in some key respects that might matter, constitutionally.

Summary of the Argument

Because Article I, Section 10 has not been acknowledged by proponents of Bitcoin legal tender laws (and rarely referenced by opponents), no legal argument has been articulated on the constitutionality of state Bitcoin legal tender laws.

This article seeks to fill that void in the discourse by advancing the following argument:

Had Bitcoin existed at the time of the Founding, it would find itself next to "gold and silver" as permissible state tender under Article 1, Section 10.

This argument interprets Article I, Section 10 through an "originalist" perspective, seeking to understand the Framers' and Ratifiers' original intent behind the section's wording. Originalism is the dominant form of constitutional interpretation today, and thus, to succeed, any argument in favor of state Bitcoin legal tender laws must engage in this form of analysis at some level.

This introductory post serves as Part I of the complete article.

Part II of this article will set forth the argument for why state Bitcoin tender laws are constitutional. Article I, Section 10’s original intent will be established by examining the colonial history of legal tender laws, as well as the Founders’ lived experience with tender laws during the Revolution and under the Articles of the Confederacy. And, crucially, the Founders own understanding of Article I, Section 10 will be explored. The historical record establishes that the Founders were chiefly concerned with fiat paper money legal tender laws, which had caused periods of rampant inflation in the nascent and early Republic.

This original intent will be synthesized with an analysis of Bitcoin’s properties. Bitcoin possesses that aspect of gold prized by the Founders: a limited supply immune to political whims. As proponents of sound money, the Founders would have had no qualms about allowing states to declare Bitcoin legal tender.

Part III will provide the counter-argument, based on a strict textualist reading of Article I, Section 10, as well as a rebuttal.

Part IV will depart from the legal analysis and focus on the policy implications of Bitcoin legal tender laws. Constitutionality aside, legal tender laws are contrary to the free market philosophical and economic theories underpinning Bitcoin. Such laws are not innocuous.

Indeed, proponents of Bitcoin's adoption as legal tender should question whether legal tender status is worth achieving. The ethos of Bitcoin is voluntarism. A frequently stated goal of Bitcoiners is to "separate money from the state." Query how this goal is accomplished through state laws mandating Bitcoin's acceptance in discharge of debts, let alone in every spot transaction, as in El Salvador.

And, once tender laws mandate Bitcoin in discharge of debts, it's a small step towards mandating Bitcoin in all transactions. (Indeed, there are sitting Senators who have proposed compulsory tender laws related to cash transactions.) The resentment that legal tender laws could create may well outweigh any possible gains in adoption.

Part II will release next week (coinciding with the start of Bitcoin 2022!). If you’d like to join me on this journey through American history, constitutional law, economics and philosophy, subscribe to the newsletter to receive each part in your inbox as it’s released.

Until next week,

Aaron

[1] Daniel Stabile and Kimberly Prior, El Salvador’s “Bitcoin Law” Forces Governments and Businesses to Contend with Digital Assets, Global Banking and Finance Review, https://www.globalbankingandfinance.com/el-salvadors-bitcoin-law-forces-governments-and-businesses-to-contend-with-digital-assets/amp/#_ftn1 (last visited Mar. 31, 2022).

[2] See https://bitcoinmagazine.com/markets/bill-introduced-to-make-bitcoin-a-legal-tender-in-arizona; and https://bitcoinmagazine.com/markets/new-bill-would-let-california-state-agencies-accept-bitcoin.

[3] https://www.azleg.gov/legtext/55leg/2R/bills/SB1341P.pdf.

[4] Arthur Nussbaum, Basic Monetary Conceptions in Law, 35 Mich. L. Rev. 865, 893 (1937).

[5] See Stabile and Prior, supra note 1.

[6] See Nussbaum, supra note 4, at 895 (referencing various compulsory laws, including those concerning American “continentals,” and the latin civil codes), and 898 ("up to the eighteenth century … proclamation of a novel coin by the sovereign meant compulsion upon the subjects to receive it to the prescribed value").